Off-Payroll Working Rules for Agency Freelancers: Updated IR35 Guidance 2025

Marketing agencies operate in one of the most challenging sectors for IR35 compliance. The project-based nature of agency work, combined with the need for specialised creative and technical skills, means most agencies rely heavily on freelance talent. This dependency makes IR35 compliance both critical and complex.

The off-payroll working rules place the responsibility for determining employment status squarely on medium and large companies engaging contractors. If you get the determination wrong, you face the full employment tax liability - potentially 25-30% additional costs on what you thought was a freelance arrangement.

Recent HMRC updates have tightened guidance around creative industries, digital marketing, and project-based work. The changes particularly affect agencies because they address common working patterns in our sector: dedicated account teams, ongoing client relationships, and integrated project delivery.

What Are The 2025 CEST Tool Updates

HMRC's Check Employment Status for Tax (CEST) tool received significant updates in early 2025, with changes that directly impact how agencies should assess freelancer relationships.

Key Changes in the Updated Tool:

The most significant change involves how CEST evaluates "control" in creative and project management roles. The tool now includes specific questions about creative direction, client relationship management, and project ownership that better reflect modern agency operations.

New Creative Industry Questions:

- Who determines the creative direction and final output?

- Does the contractor manage direct client relationships?

- Are project timelines and deliverables solely determined by the contractor?

- Does the contractor have authority over project budgets and resource allocation?

These additions help distinguish between contractors providing specific services under agency direction versus those operating as independent creative consultants.

Updated Integration Questions:

The tool now explores integration more sophisticatedly, particularly around:

- Access to internal agency systems and processes

- Participation in agency training and development programs

- Inclusion in agency social events and team activities

- Use of agency branding and marketing materials

CEST 2025 includes more detailed scenarios around substitution rights, recognising that creative work often requires specific individual skills while still allowing for legitimate substitution arrangements.

Determination Statements: Getting Them Right

Your determination statement is your primary defense against IR35 challenges. It must demonstrate that you've properly considered all relevant factors and reached a reasonable conclusion about employment status.

Essential Elements of Strong Determination Statements:

Effective determination statements require supporting evidence beyond CEST results. This includes contracts, working pattern records, email communications, and project management documentation that demonstrates the reality of the working relationship.

The statement should address any factors that might suggest employment status and explain why, despite these factors, the overall relationship remains genuinely self-employed. This balanced approach demonstrates proper consideration and reduces challenge risk.

Common Determination Statement Errors:

Many agencies create determination statements that focus only on factors supporting contractor status while ignoring employment indicators. HMRC expects balanced analysis acknowledging all relevant factors. Similarly, generic statements that don't reflect the specific working arrangements of individual contractors provide weak protection during audits.

Working Arrangements That Trigger IR35

Certain working patterns commonly found in agencies create particular IR35 risks. Understanding these triggers helps structure relationships to minimise employment status risks.

High-Risk Agency Arrangements:

Dedicated Account Management: Contractors who manage specific client accounts exclusively, attend regular client meetings as agency representatives, and have ongoing responsibility for client relationships often fall within IR35. The key indicators are exclusivity, ongoing responsibility, and client-facing authority.

Integrated Creative Teams: Freelancers who work as part of integrated creative teams, use agency creative processes and systems, and produce work under agency creative direction face higher IR35 risk. The integration into agency operations and lack of creative autonomy are primary concerns.

Long-term Retainer Arrangements: Contractors on ongoing monthly retainers, particularly those working set days or hours, with regular review meetings and integrated planning, often resemble employment relationships more than genuine freelance engagements.

Medium-Risk Arrangements:

Project-Based Specialists: Contractors engaged for specific projects with clear deliverables, defined timescales, and payment tied to project completion generally present lower IR35 risk, provided they maintain genuine autonomy over how work is delivered.

Technical Consultants: Specialists providing specific technical expertise, working with minimal supervision, using their own methods and tools, and delivering defined outputs typically fall outside IR35.

Lower-Risk Structures:

Output-Based Contracts: Arrangements focused on delivering specific outputs rather than providing services create stronger contractor relationships. Payment tied to deliverables rather than time, minimal supervision requirements, and contractor responsibility for methods reduce employment status risks.

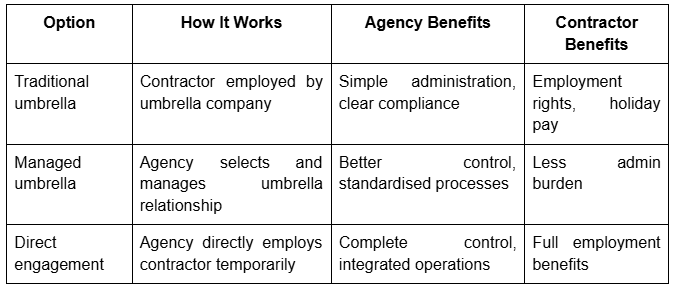

Umbrella Company Alternatives

When contractor relationships fall within IR35, agencies need compliant alternatives that work commercially for both parties. Understanding these options helps maintain access to necessary skills while ensuring tax compliance.

Umbrella Company Arrangements:

Some agencies establish their own temporary employment structures for contractors who fall within IR35. This involves either directly employing contractors for specific projects or creating subsidiary companies that handle contractor employment.

Direct employment offers maximum control but requires full payroll administration, employment law compliance, and benefit provision. Subsidiary structures can provide operational separation while maintaining administrative efficiency.

How to Manage HMRC Investigations?

Despite best efforts at compliance, agencies may face HMRC investigations into contractor relationships. Understanding the investigation process and preparation requirements helps manage these situations effectively.

Investigation Triggers:

HMRC investigations often arise from routine compliance checks, whistleblower reports, or patterns identified through data analysis. Common triggers include high contractor usage ratios, repeated long-term engagements, or inconsistent determination practices across similar relationships.

Preparation Strategies:

Maintain investigation-ready documentation that clearly demonstrates your determination process, working arrangement evidence, and compliance efforts. This includes organised file systems, readily accessible contracts and communications, and clear audit trails for all determination decisions.

Response Management:

When facing investigation, focus on demonstrating systematic compliance efforts rather than defending individual determinations. HMRC generally responds positively to evidence of genuine compliance attempts, even where individual determinations might be questioned.

The key is showing that you've made reasonable efforts to comply with the legislation based on available guidance and tools, maintaining proper documentation, and responding promptly to any identified issues.

When Investigations Lead to Disagreements:

Sometimes, despite your best compliance efforts, HMRC may reach different conclusions about contractor status or challenge your determination decisions. When this happens, you have several options for challenging their assessment and protecting your position.

Understanding your rights and the formal dispute process can make the difference between accepting an incorrect assessment and successfully defending your compliant arrangements. Read our comprehensive guide on challenging HMRC decisions and protecting your agency's interests.

Integration with Broader Employment Strategy

IR35 compliance should integrate with your broader employment and resource planning strategy rather than being treated as a separate compliance exercise.

Success requires treating IR35 compliance as a core business process rather than an annual tax exercise. Regular assessment, proper documentation, and integration with broader workforce planning ensures compliance while supporting commercial objectives.

The 2025 updates to guidance and tools provide clearer frameworks for assessment, but they also require agencies to update their compliance approaches accordingly. Staying current with these changes and implementing robust assessment processes protects against penalties while maintaining operational flexibility.

Frequently Asked Questions

Read more insights

Back to insights.jpg)

Sign up to our newsletter

Get the latest agency insights straight to your inbox