International Expansion: Financial Planning Framework for UK Agencies

Your agency has established a strong UK presence. Clients are asking for international support. Opportunities in new markets look compelling. But international expansion without proper financial planning can turn promising growth into an expensive mistake.

The agencies that succeed internationally don't just replicate their UK operations elsewhere—they build deliberate structures that optimise tax, manage compliance complexity, and create sustainable operations across jurisdictions.

The difference between profitable international growth and costly experiments lies in the planning that happens before you commit resources.

Why International Financial Planning Matters

Operating across borders introduces complexity that doesn't exist in domestic business. Different tax systems, varying compliance requirements, foreign exchange exposure, and cross-border transaction rules all affect profitability in ways that aren't immediately obvious.

A client relationship that generates healthy margins in the UK might become marginally profitable or even loss-making when delivered through an overseas office. Local corporate tax obligations, withholding taxes on cross-border payments, transfer pricing requirements, dual compliance costs, currency conversion losses, and additional administrative overhead all erode margins quietly.

Early financial planning identifies these impacts before you commit to expansion, allowing you to structure operations for optimal outcomes rather than discovering problems after you've established an overseas presence.

Assessing International Readiness

Before exploring expansion structures, honest evaluation of your agency's readiness prevents premature moves that consume resources without generating returns.

Financial Foundations

Strong financial position in the UK provides the foundation for international expansion. Agencies struggling with domestic profitability often hope international growth will solve underlying problems, but in reality, it rarely does. Sufficient capital reserves cover setup costs, initial operating losses, and unexpected complications. International expansion typically requires 12-18 months before new operations reach profitability.

Proven international demand from existing clients reduces market risk. If UK-based clients aren't asking for international support, why will overseas clients buy your services?

Operational Capabilities

Beyond finances, operational readiness determines execution success. Can you effectively manage teams across time zones and cultures? Are your processes documented and transferable to new markets? Does your management team have capacity for expansion complexity? Can your systems support multi-currency, multi-jurisdiction operations?

These operational questions matter as much as the financial metrics. An agency with strong financials but weak systems will struggle internationally just as much as one with inadequate capital.

Structure Options for International Operations

How you structure international activities fundamentally affects tax treatment, compliance requirements, and operational flexibility.

Direct Service Provision from the UK

The simplest approach involves delivering services to international clients directly from your UK entity without establishing overseas presence. This works for occasional international projects without regular overseas presence, digital service delivery without need for local physical presence, and early testing of international markets before committing to expansion.

From a tax perspective, UK corporation tax applies to all profits, though withholding taxes may apply to certain payments from overseas clients. VAT treatment depends on client location and service type, but you avoid overseas compliance obligations unless activity creates taxable presence.

The limitations become apparent quickly. You create permanent establishment risk if overseas activity becomes significant, may face disadvantage versus local competitors in target markets, have limited ability to hold overseas contracts or employ local staff, and face currency exposure on all international transactions.

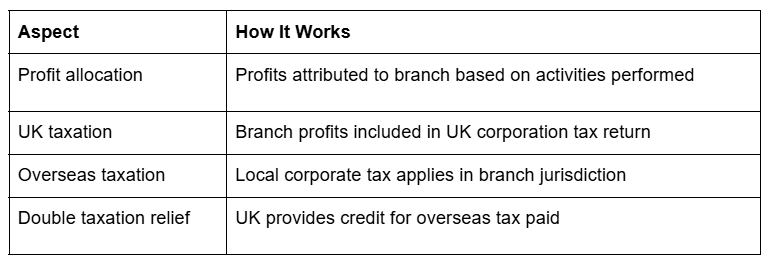

Overseas Branch Operations

A branch represents your UK company operating in another jurisdiction without creating a separate legal entity. It's not a standalone entity since activities and liabilities belong to your UK parent company, though local registration is typically required.

Tax treatment works as follows:

Branches make sense for testing markets before committing to subsidiary structure, jurisdictions where branches receive favourable treatment, temporary or project-based overseas presence, and operations where group loss relief benefits matter.

The drawbacks include potentially complex profit allocation requirements, possibly less credibility than local subsidiary in some markets, and complications for eventual exit or restructuring. Branch losses become immediately available for UK group relief, which can be either advantage or disadvantage depending on your circumstances.

Overseas Subsidiary Companies

Creating separate legal entities in target jurisdictions provides the most common expansion structure for established operations. You get a standalone legal entity in the overseas jurisdiction with separate corporate tax obligations, independent compliance requirements, and limited liability for the parent company.

The tax planning opportunities here become significant. Profits can remain in the subsidiary, deferring UK tax until distribution and allowing reinvestment in local operations without immediate UK tax impact. Repatriation through dividends may qualify for participation exemption, reducing or eliminating UK tax on distributions.

Intercompany transactions between UK parent and overseas subsidiaries require arm's length pricing under transfer pricing rules, creating both planning opportunities and compliance obligations. Strategic location of intellectual property ownership can optimise overall group tax position.

Subsidiaries work best for permanent presence in target markets, when you need to employ local staff, where clients prefer local entity contracts, when asset ownership requirements exist in the jurisdiction, and for long-term market commitment.

The compliance burden increases substantially with separate corporate tax returns in each jurisdiction, local accounting and audit requirements, annual filings and governance obligations, transfer pricing documentation, and consolidated group reporting requirements.

Partnership and Joint Venture Structures

Collaborative arrangements with local partners offer alternative expansion models, particularly for market entry. These range from formal legal partnerships to joint venture companies with local partners, associate relationships and network arrangements, or strategic alliances without equity sharing.

Partnership structures typically share profits according to agreed formulae, affecting both tax treatment and commercial returns. Profit split arrangements require careful documentation to withstand tax authority scrutiny. Joint venture companies create separate entities with shared ownership, combining subsidiary benefits with local partner expertise and market access.

The risk factors centre on relationships rather than structures. Partner relationship quality determines success more than legal form, profit sharing reduces returns compared to wholly-owned operations, exit becomes complex if relationships deteriorate, and potential for disputes over strategy, investment, and operations remains ever-present.

Tax Implications Across Structures

Understanding tax impacts helps evaluate true profitability of international operations and informs structure decisions.

Corporate Income Tax Considerations

Each jurisdiction applies corporate income tax to profits arising within its borders, but rules for determining what constitutes local-source profit vary significantly. Permanent establishment creates local tax obligations and arises through fixed place of business in the jurisdiction, dependent agents acting on company's behalf, or certain construction or service activities exceeding time thresholds.

Once PE exists, a portion of company profits becomes taxable in that jurisdiction even without a separate legal entity. This catches many agencies unprepared.

Tax rate variations affect structure decisions fundamentally:

Withholding Taxes on Cross-Border Payments

Many countries impose withholding tax on payments made to overseas entities for services, royalties, or interest. Rates typically range from 0-30% depending on payment type, applicable tax treaties between countries, and recipient entity structure and location.

Review tax treaties to identify beneficial routing options, structure payments to minimise withholding tax exposure, claim treaty benefits through proper documentation, and consider substance requirements for treaty access.

Value Added Tax and Indirect Taxes

Cross-border services face complex VAT treatment depending on service type, client location, and business-to-business versus business-to-consumer classification.

For B2B services to EU clients, generally reverse charge applies—the client accounts for VAT rather than the supplier charging it. For B2B services to non-EU clients, services are typically outside scope of VAT, though local indirect taxes may apply in client jurisdiction. Digital services to consumers trigger special rules, potentially requiring registration in customer's location.

VAT planning becomes particularly important when expansion involves physical presence, as this may trigger local VAT registration requirements independently of corporate tax considerations.

Transfer Pricing: The Compliance Burden

Once you operate through multiple entities, transfer pricing rules govern how you price transactions between connected companies. This affects both compliance costs and tax outcomes in ways that surprise most agencies.

Any transaction between related entities requires arm's length pricing—the price independent parties would agree in comparable circumstances. This covers management services between parent and subsidiary, service delivery between group entities, cost recharges and shared services, intellectual property licensing, and intercompany loans and financing.

Tax authorities increasingly demand substantial documentation supporting transfer pricing positions. The master file describes overall group structure, operations, business strategy, and transfer pricing methodology. The local file provides detailed analysis of specific transactions and benchmarking evidence supporting pricing. Country-by-country reporting requires large groups to report revenues, profits, taxes paid, and employees in each jurisdiction globally.

When to Seek Professional Guidance

International expansion complexity warrants specialist advice earlier rather than later. DIY approaches often create problems requiring expensive unpicking.

Engage advisers when initial structure design determines tax outcomes for years, transfer pricing requirements apply, multiple jurisdictions are involved, significant IP or valuable assets exist, or complex group structures already exist. The cost of proper planning typically represents 2-5% of initial setup investment but can save multiples of this through better structure and avoided mistakes.

Planning international expansion for your agency?

Our team can help you in international tax planning and structure design for service businesses. We can help you evaluate options, design optimal structures, and navigate the compliance complexity of global operations.

Book a consultation to discuss your expansion plans and ensure your international growth creates value rather than consuming it.

Frequently Asked Questions

Read more insights

Back to insights

Sign up to our newsletter

Get the latest agency insights straight to your inbox