Working from Abroad as a UK Agency Director (Complete Tax Guide 2025)

You've built a successful UK marketing agency, and now you're thinking about working from that villa in Spain or your partner's family home in France for a few months. After all, you just need an internet connection and your laptop, right?

Not quite.

Working abroad as a UK agency director isn't as simple as packing your laptop and hoping for good WiFi. The tax implications alone can be complex, and that's before you consider social security, employment law, and potential permanent establishment risks for your agency.

Agency directors make costly mistakes by not understanding the rules. Some ended up with unexpected tax bills in multiple countries, while others inadvertently created tax obligations for their agencies abroad. The worst case I dealt with involved an agency director who moved 8 months in Dubai and triggered a £40,000 corporation tax bill for his agency – completely avoidable with proper planning.

Here's everything you need to know about working from abroad as a UK agency director in 2025.

The Reality of Remote Agency Management

Since the pandemic, many agency directors have embraced location independence. It's tempting – manage your team via Zoom, handle client relationships digitally, and enjoy better weather while doing it. The technology makes it feel seamless, and for many day-to-day operations, it genuinely is.

But what most directors don't realise is that even temporary overseas work can trigger serious tax and legal consequences for both you personally and your agency. The key is understanding how long you plan to be away, because duration changes everything. What's perfectly fine for a two-week working holiday can become a compliance nightmare if it extends to six months.

Think of it like this: tax authorities don't care that you're still serving UK clients or that your team is based in Manchester. They care about where you are when you're making business decisions, signing contracts, or performing the core functions of your role as director.

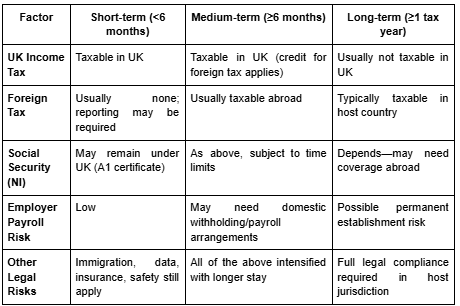

Tax Implications by Duration Abroad

Short-Term (Under 6 Months)

For shorter overseas stints, the tax picture is relatively straightforward. You remain taxable in the UK on all your income – your director's salary, dividends, and any other UK source income continues to be taxed exactly as if you'd never left. Most countries won't tax you on your UK employment income if you're there for less than six months, though some may require you to file a tax return declaring your income even if no tax is due.

Your agency faces minimal risk of creating overseas tax obligations during short-term periods. You can continue operating UK payroll as normal, and the permanent establishment risk is generally low, provided you're not actively soliciting new business or making major strategic decisions while abroad.

Medium-Term (6 Months or More)

Once you cross the six-month threshold, complexity increases significantly. You're still taxable in the UK on your director's remuneration, but you'll likely become taxable in the host country too. The good news is that double taxation agreements usually prevent you from paying tax twice on the same income – you can typically claim a foreign tax credit in the UK for any tax paid abroad.

However, you may need to register for tax in the overseas jurisdiction, file local tax returns, and potentially make advance payments if you become tax resident there. Each country has different rules for determining tax residence, and some can catch you as early as 90 days.

Your agency also faces increased risks. Extended director presence abroad raises the specter of permanent establishment – essentially creating a taxable presence for your UK company in the foreign country. This could mean local corporation tax registration, ongoing compliance obligations, and additional accounting costs.

Long-Term (One Full UK Tax Year or More)

Extended periods abroad can fundamentally change your tax position. You may lose UK tax residence status entirely, meaning your UK employment income could become non-taxable in the UK. Instead, you'd be fully taxable in the host country on all your worldwide income, including your UK director's remuneration.

The permanent establishment risk for your agency becomes almost inevitable with long-term overseas presence. If you're actively managing the business from abroad for a full tax year, most countries would consider this sufficient to create a local taxable presence. This means potential corporation tax registration, local accounting requirements, and ongoing compliance costs that could easily reach thousands of pounds annually.

There's also the question of what happens when you eventually return to the UK. Resuming UK tax residence can be complex, particularly if you've been non-resident for several years.

The Risk from Permanent Establishment

If you're actively managing your agency from abroad, you could inadvertently create a permanent establishment for your UK company in the host country. This includes making strategic decisions, signing contracts, negotiating with clients, or substantially managing day-to-day operations. Even working from a home office abroad can create permanent establishment if you're performing core business functions there regularly.

The consequences are serious. Your agency becomes liable for corporation tax in the host country on profits attributable to that permanent establishment. You'll need local tax registration, potentially local accounting standards compliance, and ongoing tax filings. Some countries impose penalties for late registration that can reach tens of thousands of pounds.

Higher risk activities include:

- Meeting clients face-to-face in the host country

- Signing contracts while abroad

- Making significant business decisions overseas

- Negotiating deals or partnerships

- Having a fixed place of business (even a home office used regularly)

Lower risk approaches involve:

- Delegating major decisions to UK-based team members

- Avoiding client meetings in the host country

- Keeping your role to oversight and communication only

- Ensuring contracts are signed by UK-based directors

- Limiting your activities to routine administrative tasks

Social Security and National Insurance Considerations

Income tax gets most of the attention, but social security coordination can be equally important and is often completely overlooked. The rules here are different from income tax and depend heavily on whether your destination has a social security agreement with the UK.

For EU and EEA countries, you might be able to remain under UK National Insurance using an A1 certificate. This is particularly relevant if your agency "sends" you abroad rather than you choosing to go independently. The distinction matters because being "posted" by your employer often allows you to stay under home country social security rules.

Post-Brexit, the UK-EU protocol still covers social security coordination, but UK National Insurance coverage abroad is now limited to a maximum of 2 years. After that, you'd typically need to join the local social security system.

For non-EU countries, check whether the UK has a bilateral social security agreement with your destination. Without such an agreement, you could end up paying social security contributions in both countries – UK National Insurance plus local social security. This can add significant cost, particularly in countries with high social security rates.

The key is planning ahead. Apply for any necessary certificates before you travel, as trying to sort this out retrospectively is much more difficult and expensive.

Tax-Efficient Planning Strategies

Optimise Your Remuneration Mix

If you're planning an extended period abroad, consider adjusting your remuneration strategy. Taking more salary (which is deductible for the company) versus dividends might be beneficial, particularly if the destination country taxes employment income more favorably than investment income, or vice versa.

Timing dividend payments can also be crucial. If you're likely to become tax resident abroad, consider taking dividends before departure or after return to the UK, depending on the relative tax rates.

Pension contributions deserve special attention. Maximising pension contributions before departure can provide valuable UK tax relief while potentially reducing your taxable income in the destination country.

Plan Your Tax Residence Carefully

The UK's Statutory Residence Test provides a framework for determining tax residence, but it's complex and fact-specific. Key factors include the number of days spent in the UK, your accommodation ties, work ties, and family connections.

If you're planning a long-term move, understanding these rules can help you manage your tax residence status strategically. Sometimes an extra week in the UK, or avoiding it entirely, can make the difference between being UK tax resident or not.

For destination countries, research their tax residence rules carefully. Some countries have automatic residence tests based purely on days present, while others look at broader factors like family, economic ties, or having a permanent home available.

Tax Implications by Duration

When to Seek Professional Help

The complexity of cross-border tax means professional advice often pays for itself. You definitely need specialist help if you're planning to work abroad for more than three months, considering a permanent move, have clients in the destination country, or your agency has significant overseas activities.

Don't try to navigate this alone, particularly for medium or long-term arrangements. The cost of getting it wrong – both financially and in terms of compliance headaches – far exceeds the cost of proper planning.

Look for advisers who specialise in expatriate tax and have experience with your destination country. General tax advisers often lack the specialised knowledge needed for cross-border scenarios.

Need Help Planning Your Overseas Work Strategy?

If you're considering working abroad while running your UK agency, let's discuss how to structure this tax-efficiently and compliantly.

Book a strategy call where we'll review your specific situation and travel plans, and identify potential tax and legal risk

Frequently Asked Questions

Read more insights

Back to insights

Sign up to our newsletter

Get the latest agency insights straight to your inbox