UK November 2025 Budget: Complete Guide to Tax Changes for Businesses

The UK November 2025 Budget has delivered one of the largest tax increases in recent years, with the Chancellor raising £26.1 billion annually through strategic changes that predominantly take effect from 2027 onwards.

Unlike previous budgets focused on headline rate changes, this announcement centres on threshold freezes and targeted adjustments designed to gradually increase the tax burden while giving businesses time to plan ahead.

Here's everything you need to know about the key measures and their implementation timeline.

Income Tax and National Insurance Changes

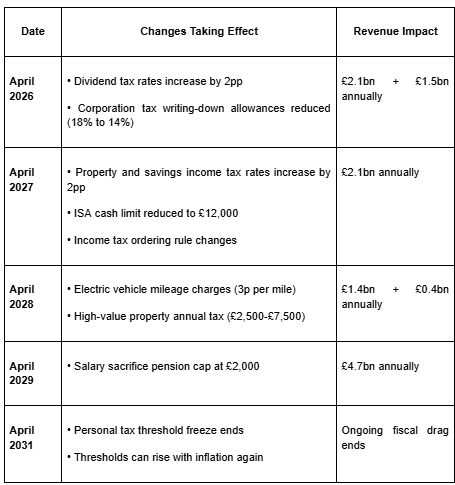

Personal Tax Threshold Freeze Extended to 2031

The most significant revenue-raising measure extends the personal tax threshold freeze for an additional three years until April 2031. This builds on previous freezes and represents what economists call "fiscal drag" - a method of increasing tax revenue without raising headline rates.

Key Details:

- Personal allowance remains frozen at £12,570

- Higher rate threshold stays at £50,270

- Additional rate threshold unchanged at £125,140

- Revenue impact: £8.0 billion annually by 2029-30

Business Impact: The Office for Budget Responsibility projects this will pull 780,000 more people into basic rate tax and 920,000 into higher rate tax by 2029-30. For businesses, this affects salary benchmarking, bonus planning, and decisions around director remuneration strategies.

Pension Contribution Reforms

Salary Sacrifice Cap Introduced

From April 2029, pension contributions made through salary sacrifice arrangements face significant restrictions, fundamentally altering workplace pension planning.

The Change:

- Only the first £2,000 annually of salary sacrifice pension contributions remains National Insurance exempt

- Contributions above £2,000 attract both employer and employee National Insurance

- Revenue impact: £4.7 billion annually by 2029-30

Critical Distinction: This change applies solely to salary sacrifice arrangements. Direct employer pension contributions made by the company remain completely unaffected, potentially making them more attractive for business owners and high earners.

Investment Income Tax Increases

Dividend, Property and Savings Income Rates Rise

The government introduces separate tax rates for different types of investment income, with increases of 2 percentage points across most bands from April 2027.

Dividend Tax Changes (April 2026):

- Basic rate: 8.75% to 10.75%

- Higher rate: 33.75% to 35.75%

- Additional rate: remains 39.35%

Property and Savings Tax Changes (April 2027):

- Basic rate: 20% to 22%

- Higher rate: 40% to 42%

- Additional rate: 45% to 47%

Revenue impact: £2.1 billion annually

Business Implications: These changes particularly affect company directors who extract profits via dividends, property investors, and businesses with significant cash reserves earning interest. The government data shows only 9% of taxpayers receive taxable dividend income, making this a targeted measure.

Corporation Tax Updates

Rates Unchanged, Allowances Reduced

While the main Corporation Tax rate remains at 25%, changes to capital allowances affect business investment planning.

Key Changes:

- Corporation Tax rate: stays at 25%

- Writing-down allowances: reduced from 18% to 14% from April 2026

- New 40% first-year allowance introduced from January 2026

- Full expensing unchanged

- Revenue impact: £1.5 billion annually

The reduction in writing-down allowances means businesses receive less tax relief on capital expenditure over time, potentially influencing investment timing and asset purchase decisions.

Electric Vehicle Taxation

Mileage-Based Charging Introduced

A new approach to electric vehicle taxation launches in April 2028, replacing the current exemption with mileage-based charges.

The New System:

- Battery electric vehicles: 3p per mile

- Plug-in hybrids: 1.5p per mile

- Collection via annual MOT mileage readings

- Revenue impact: £1.4 billion by 2029-30

For businesses operating electric vehicle fleets, this represents a significant new cost. A vehicle covering 20,000 miles annually faces charges of £600, compared to zero under current arrangements.

ISA Structure Changes

Cash ISA Limits Reduced

From April 2027, the ISA system undergoes structural reform while maintaining the overall £20,000 allowance.

The Changes:

- Overall ISA allowance: remains £20,000

- Cash ISA limit: reduced to £12,000

- Stocks & Shares ISA minimum: £8,000 (of the remaining allowance)

- Over-65s retain full £20,000 cash allowance

This particularly affects business owners who prefer cash-based savings for emergency funds or short-term business investment opportunities.

Property Tax Reforms

High-Value Property Annual Charge

A new annual tax targets expensive residential properties from April 2028.

The Structure:

- Properties £2-5 million: £2,500 annually

- Properties £5 million+: £7,500 annually

- Collection via local authorities

- Revenue impact: £400 million annually

Economists suggest this annual charge could reduce property values by 4-6% due to capitalisation effects, with a £7,500 annual charge potentially reducing a £5 million property's value by £200,000-£300,000.

What Didn't Change

Several widely rumored changes failed to materialise:

- Capital Gains Tax rates: unchanged

- Business Asset Disposal Relief: no modifications

- VAT registration threshold: remains £85,000

- Inheritance tax reliefs: no changes

- Exit taxes: no new measures introduced

- Stamp duty: no additional changes for 2027

Implementation Timeline

Economic Context

The Budget represents a fundamental shift in UK tax policy, with the tax-to-GDP ratio reaching an all-time high of 38.3% by 2030-31. The OBR describes this as representing a 5 percentage point increase from pre-pandemic levels and the third-largest tax increase since 2010.

GDP growth forecasts have been revised to 1.5% for 2025, with productivity growth expectations reduced to 1.0% from 1.3%, reflecting the economic impact of these fiscal measures.

HMRC Compliance Focus

The Budget includes substantial increases in HMRC compliance funding, with additional resources allocated to investigations and enforcement activities. This signals more enquiries targeting businesses and high-earning individuals over the coming years, making accurate record-keeping and proactive tax planning even more crucial.

Next Steps for Your Business

Staying informed of these changes is the first step in effective tax planning. The extended timeline provides opportunities for strategic preparation, but successful navigation requires careful consideration of your specific circumstances.

If you'd like to discuss how these Budget changes affect your business and explore optimisation strategies, book a consultation to review your situation with a specialist who understands the complexities of business tax planning.

Frequently Asked Questions

Read more insights

Back to insights

.jpg)

Sign up to our newsletter

Get the latest agency insights straight to your inbox