Running an agency comes with countless decisions, but few impact your personal finances as much as how you pay yourself. Many agency owners I work with initially focus all their energy on growing revenue while overlooking how efficiently they extract that hard-earned money from their business.

The difference between an optimised and sub-optimal remuneration strategy can easily amount to thousands of pounds in unnecessary tax each year. That's money that could otherwise fund your next holiday, home renovation, or boost your retirement savings.

Let's cut through the complexity and outline exactly how to structure your income in the most tax-efficient way for the 2026/27 tax year.

Understanding the Basics: Salary vs. Dividends

Before diving into specific strategies, you need to understand the two primary ways to pay yourself as an agency owner:

Salary is a fixed payment from your business to you as an employee or director. It's subject to Income Tax and National Insurance Contributions (NICs) for both you and your company.

Dividends are distributions of company profits to shareholders. They're taxed differently than salary and aren't subject to NICs, which creates significant potential tax advantages.

The key difference lies in how these payments affect your company's finances. Salary is a business expense that reduces your company's taxable profit, while dividends can only be paid from post-tax profits after Corporation Tax has been deducted.

How Salary is Taxed in 2026/27

When taking salary, both you and your company face tax implications:

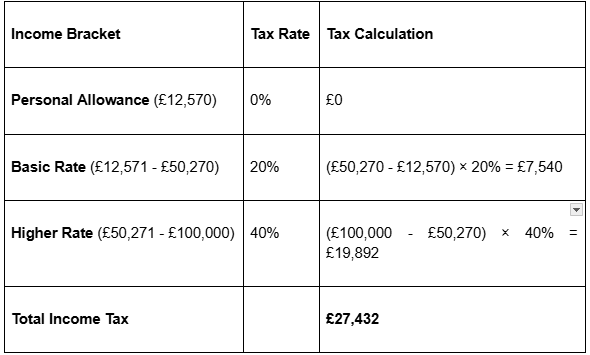

Income Tax Bands for 2026/27

- Personal Allowance: £12,570 (tax-free income)

- Basic Rate (20%): £12,571 – £50,270

- Higher Rate (40%): £50,271 – £125,140

- Additional Rate (45%): £125,141+

National Insurance Contributions (NICs) 2026/27

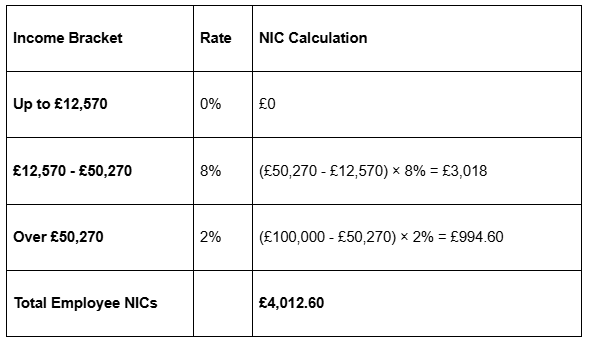

Employee NICs:

- 8% on earnings between £242 and £967 per week

- 2% on earnings above £967 per week

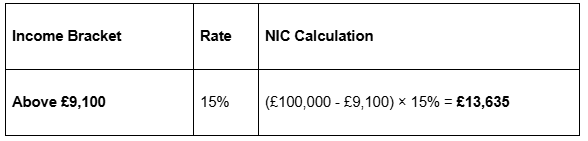

Employer NICs:

- 15% on salaries above £96 per week (increased from 13.8% in 2024/25)

Taking salary does provide important benefits: it qualifies for state pension accrual, contributes to other state benefits like maternity pay, and demonstrates regular income for mortgage applications. However, the combined burden of Income Tax and NICs makes salary less tax-efficient than dividends for extracting profits.

How Dividends Are Taxed in 2026/27

Dividends have a different tax treatment that often makes them more attractive:

- Dividends are paid from post-tax profits (after the 25% Corporation Tax)

- Dividend Allowance: £500 tax-free (significantly reduced from £5,000 several years ago)

- Dividend Tax Rates:

- Basic Rate: 10.75% (on dividends within basic income tax band)

- Higher Rate: 35.75% (on dividends within higher income tax band)

- Additional Rate: 39.35% (on dividends above £125,140)

The primary advantage of dividends is that they aren't subject to NICs, which creates immediate savings. However, remember that dividends can only be legally distributed if your company has sufficient profits after tax.

The Most Tax-Efficient Salary & Dividend Split in 2026/27

For most agency owners, the optimal approach combines salary and dividends strategically.

The Most Common Strategy:

- Pay yourself a salary of £12,570 per year (£1,047.50 monthly)

- Take remaining income as dividends

This approach maximises tax efficiency because:

- The £12,570 salary uses your full Personal Allowance (completely tax-free)

- It stays below the National Insurance threshold, avoiding employee and employer NICs

- It's sufficient to maintain state pension qualification

- Additional income comes via dividends taxed at lower rates than equivalent salary

Example Calculation for £100,000 Income

Option 1: £100,000 as salary

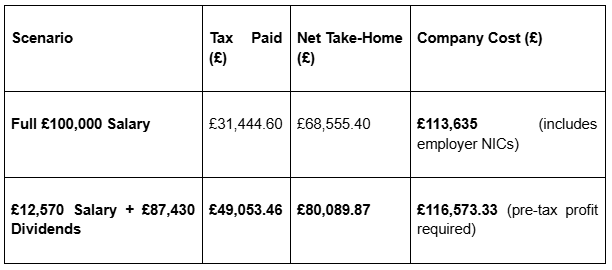

Let's compare how taking £100,000 as pure salary versus the optimised salary/dividend split affects your take-home pay:

Step 1: Income Tax Calculation

Step 2: National Insurance Contributions (NICs)

Employee NICs (Paid by You)

Employer NICs (Paid by Your Company)

Note: Employer NICs do not come out of your salary but are an additional cost to the company.

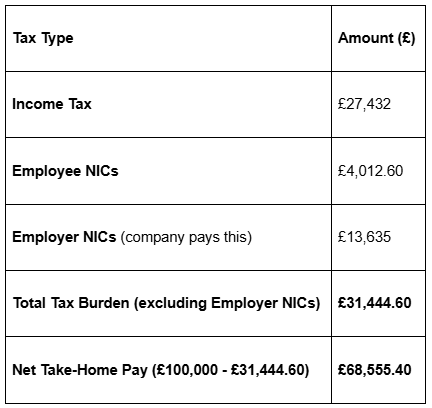

Step 3: Total Tax Burden & Net Take-Home Pay

If you take the entire £100,000 as salary, you pay £31,444.60 in tax and NICs, leaving you with £68,555.40 net.

Your company also incurs an additional £13,635 in employer NICs, making the total cost £113,635.

Option 2: Optimised split (£12,570 salary + £87,430 dividends)

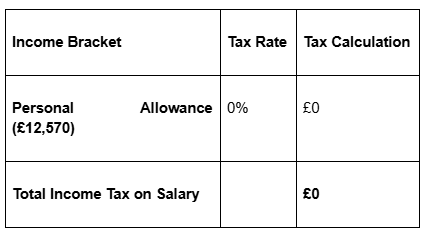

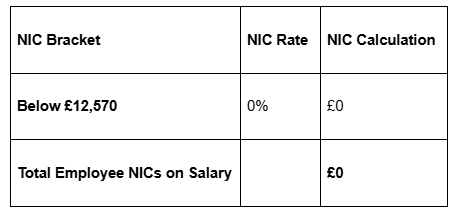

Step 1: Tax on Salary (£12,570)

Since the salary is £12,570, it’s covered by the Personal Allowance (no Income Tax) and falls below the National Insurance threshold (no NICs).

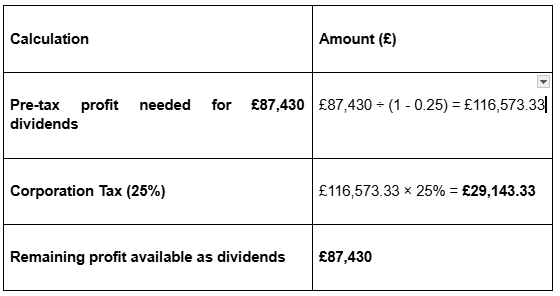

Step 2: Corporation Tax on Dividends

Dividends are paid from post-tax profits, meaning we need to account for Corporation Tax (25%) first:

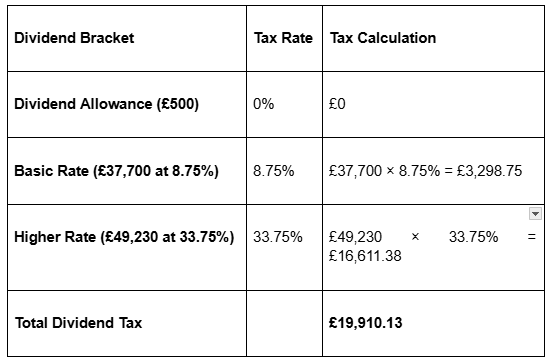

Step 3: Dividend Tax

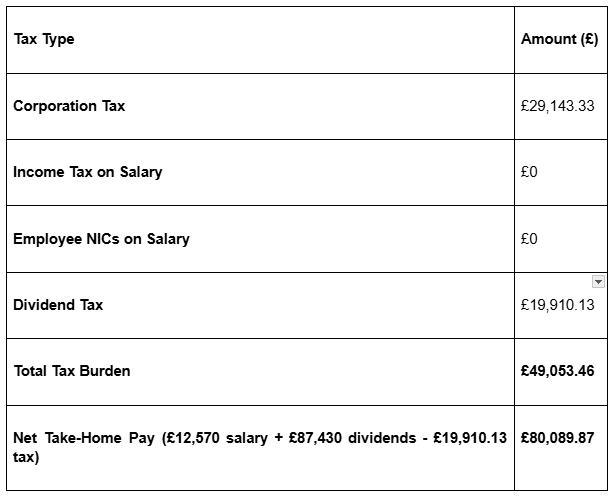

Step 4: Total Tax Burden & Net Take-Home Pay

Final Summary:

The optimised approach saves approximately £16,446 in this scenario – a substantial difference that demonstrates why proper tax planning matters.

Additional Tax-Efficient Strategies for Agency Owners

Beyond the basic salary/dividend split, consider these additional strategies:

Employing Family Members

If your spouse or adult children work legitimately in your business, paying them a salary uses their tax allowances. Each family member can receive up to £12,570 tax-free, potentially saving thousands in family tax.

However, HMRC requires that:

- The work is genuine and necessary

- Pay rates are commercially reasonable

- Proper documentation exists (contracts, timesheets, etc.)

Director's Pension Contributions

Company contributions to your pension are:

- Tax-deductible for your business (reducing Corporation Tax)

- Not subject to Income Tax or NICs

- Not counted toward your annual allowance limit if made directly by the company

This creates a triple tax advantage, making pension contributions one of the most tax-efficient ways to extract value.

Company Expenses & Benefits

Legitimate business expenses that have a personal benefit can include:

- Home office allowance (£6 per week without receipts)

- Mileage allowance for business travel (45p per mile for the first 10,000 miles)

- Mobile phone and broadband (if there's a business need)

- Professional subscriptions and training

When to Prioritise Salary Over Dividends

While dividends are generally more tax-efficient, certain situations favor taking more salary:

- Mortgage Applications: Lenders typically prefer to see steady salary income rather than dividends. If you're planning to apply for a mortgage, consider increasing your salary temporarily.

- Limited Company Profits: Dividends can only be legally paid from available profits. If your agency has limited profitability, salary might be your only option.

- Pension Planning: Employer pension contributions are based on salary. Higher salary levels allow for larger employer pension contributions.

- Loss-Making Periods: During challenging periods, salary remains deductible even if the company is making losses, whereas dividends cannot be paid from non-existent profits.

Common Mistakes to Avoid

Paying Too Little Salary

While minimising salary seems advantageous, taking less than £6,240 annually affects your state pension eligibility. Consider the long-term impact beyond immediate tax savings.

Illegal Dividend Declarations

Paying dividends without sufficient profits is illegal and can lead to:

- Personal liability for the dividends

- HMRC penalties and investigations

- Legal complications if the company faces financial difficulties

Always confirm available profits with your accountant before declaring dividends.

Ignoring Higher Tax Thresholds

Large dividend payments can push you into higher tax brackets. Proper timing of dividend payments across tax years can keep you in lower brackets. Sometimes, delaying a dividend by just a few days (into the next tax year) can save thousands.

Neglecting Regular Review

Tax rules change annually. What worked last year might not be optimal this year. Regular reviews with an accountant ensure your strategy remains optimal.

Planning for 2026/27: Practical Steps

For the 2026/27 tax year, take these proactive steps:

- Calculate your anticipated annual income from all sources

- Model different salary/dividend combinations to identify the most tax-efficient approach

- Consider the timing of dividend payments to optimise tax bands across tax years

- Review family member involvement in your business

- Evaluate pension contribution opportunities

- Document all decisions properly through board minutes and dividend vouchers

Making Your Money Work Harder

The difference between basic and optimised remuneration planning can be substantial. For an agency owner taking £100,000 from their business, proper planning typically saves £10,000-£20,000 annually in tax.

At Sidekick, we specialise in helping agency owners implement these strategies. Our clients benefit from proactive tax planning that evolves with changing regulations and personal circumstances.

Ready to optimise how you pay yourself and potentially save thousands in unnecessary tax? Book a consultation with our team of agency specialist accountants. We'll review your current arrangements and identify opportunities to make your money work harder for you.

Questions agency owners ask

What is the difference between salary and dividends for agency owners?

Salary is a fixed payment from your business to you as an employee or director, subject to Income Tax and National Insurance Contributions. Dividends are distributions of company profits to shareholders, taxed differently and not subject to NICs, which can provide significant tax advantages.

How is salary taxed in the 2026/27 tax year?

In the 2026/27 tax year, salary is subject to Income Tax and National Insurance Contributions. The Personal Allowance is £12,570, and salaries above this amount are taxed at different rates depending on the income band.

What are the tax advantages of taking dividends instead of salary?

Dividends are paid from post-tax profits and are not subject to National Insurance Contributions, which creates immediate savings. Additionally, there is a Dividend Allowance of £500 that is tax-free, and dividends are taxed at lower rates compared to equivalent salary.

What is the most tax-efficient way for agency owners to pay themselves?

The most tax-efficient approach for agency owners is to pay themselves a salary of £12,570 per year and take the remaining income as dividends. This strategy maximises tax efficiency by using the full Personal Allowance and avoiding National Insurance Contributions.

What common mistakes should agency owners avoid when paying themselves?

Agency owners should avoid paying too little salary, as this can affect state pension eligibility. They should also ensure dividends are only declared when there are sufficient profits, as illegal dividend declarations can lead to penalties and legal issues.